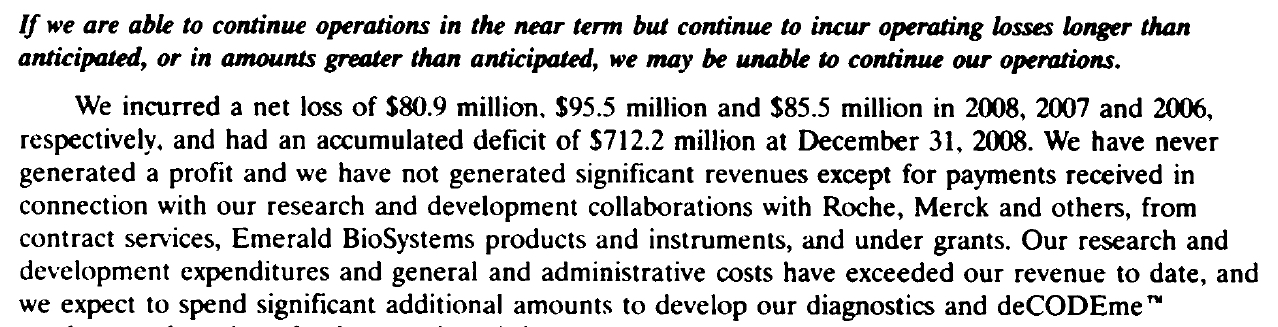

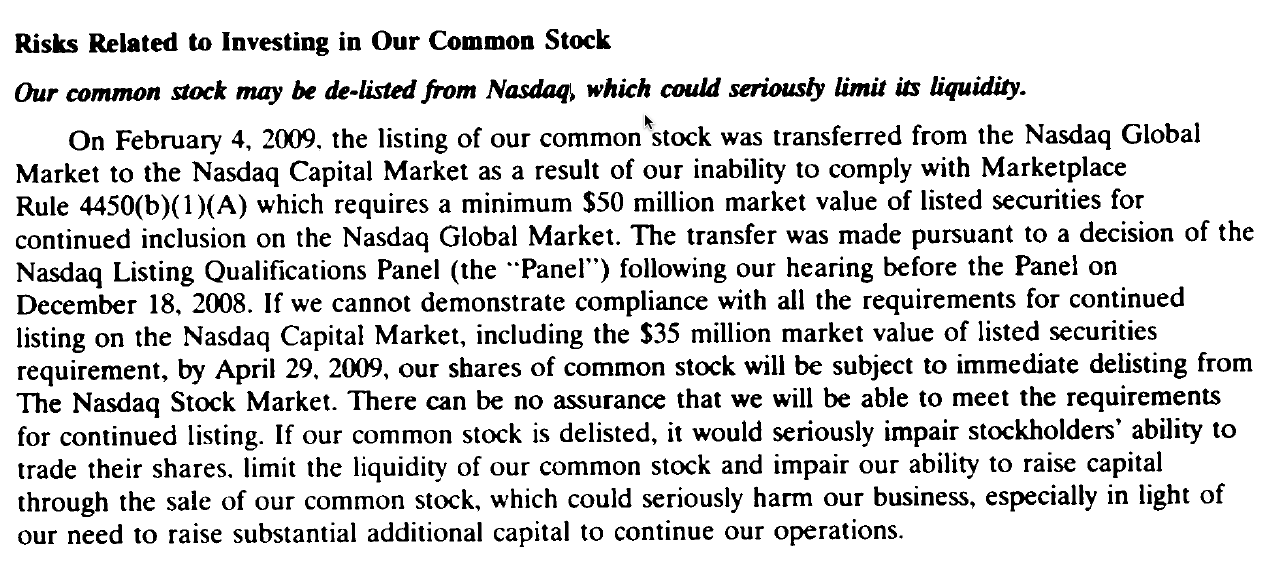

When we first saw Hannes Smárason way back in installment one, he was a dressed-up trashcan on the streets of Reykjavik, who years later had transmogrified himself into the new CEO of WuXi NextCODE, a more-or-less Chinese genomics company in the same way that deCODE Genetics (in many ways the progenitor of WuXi) had been more-or-less an Icelandic genomics company. That unexpected reappearance was what first provoked me to revisit the figure of Smárason, who had been the founding Chief Financial Officer of deCODE before finding bigger fish to fry (meaning bigger entities to bring to financial ruin) in Iceland’s FL Group. I diverged to some of the financial history of deCODE in installment two, and then began documenting its bankruptcy proceedings in installment three; that is still incomplete, but will eventually narrate how deCODE would survive as a legal-corporate entity to eventually be sold a few years later to the U.S. biotech corporation Amgen for a rather astounding sum of money (about $450 million, of which deCODE’s previous investors, including many Icelanders, would see about $0.)

I’m postponing the completion of Installment 3 in this series on Zombie Corporate Vikings even further, since there’s some material pertaining to Smárason, that Zombie Corporate Viking who started me on this whole roll, that I’ve been sitting on for a while, but that has recently come alive again through some reporting on (it is still so hard to type this) president-elect Donald Trump. I want to at least get the bare bones of this zombie corporate viking story up and shambling about, and then maybe come back and flesh it out a bit more when I have more time.

Smárason bailed from deCODE in 2000 to…well, I’ll let The Reykjavik Grapevine begin the story:

When all is said and done, it was the celebration of investment bankers and oligarchs by politicians, the fawning profiles of financiers and corporate raiders in the daily press along and the utterly uncritical celebration of “the market” as infallible, which was the real problem and the root cause of the bubble, and much of the wreckage it left in its wake.

A good example of how this works is the case of FL Group. In 2004, a former DeCode executive named Hannes Smárason gained control of the airline Icelandair with the help of Baugur and Jón Ásgeir Jóhannesson. Icelandair was at that time one of the most solid companies in Iceland, and one of few airlines in the world that was consistently profitable. Hannes set about to transform the company, changing its name to FL Group to reflect his ambitious global plans. These plans turned out to be a classic corporate raid, as Hannes sold all hard assets out of the company, leaving only cash and equity in other companies, which was then leveraged in order to turn FL Group into an “investment company”. Of course the main investments were in the financial sector—primarily in Glitnir (which was turned into a personal ATM for Jón Ásgeir and associates at a later stage in the game). The markets celebrated and the stock price of FL Group rose more than 50% in six months.

But while the business strategy of Hannes Smárason found favour with the stock market, several members of the board of directors, as well as the CEO of the company, realised that something was wrong. Within the span of six months in 2005, the majority of the board and the CEO of the company resigned without any official explanation. Hannes brushed these resignations off as the stock market gave him a vote of confidence and the price of FL Group stock continued to rise. The media saw no reason to make a fuss, and at the end of 2006 Hannes was voted “businessman of the year” by the most widely read business weekly, Fréttablaðið’s The Market (it might bear noting that Fréttablaðið is owned by the aforementioned Jón Ásgeir Jóhannesson). By then, FL Group’s stock value had more than doubled since Hannes assumed the reins.

Needless to say, FL Group was among the first firms to declare bankruptcy in 2008, its shareholders losing all their paper gains. Several questions remain unanswered about large transfers from FL Group to offshore banking accounts, and Hannes Smárason has been sued by the resolution committee of bankrupt bank Glitnir for his role, and the role of FL Group, in the looting the bank.

Smárason would face “a whole slew of cases,” including an alleged illegal loan and embezzlement, all of which he would walk away from. (His defense on the latter charge was absolutely Nixonian, according to the Iceland Monitor: “During the trial, Smárason has maintained his innocence saying that he did not remember the emails he had written at the time and that he did not remember or recognise the documents presented.” ) But let’s return to his highest-flying oligarch days, when the FL Group entered into an real estate alliance with the Bayrock Group LLC, to build Trump SoHo and several other buildings in which Trump had a 15% stake. Part of this was a Trump tax dodge, as London’s Telegraph reported:

In 2007 Bayrock struck a deal with FL Group, an Icelandic company that had agreed to invest $50 million in four of Bayrock’s subsidiary partnerships. However, the deal was later relabeled as a loan.

In New York, the sale of a stake in a partnership would make the existing partners liable to pay more than 40 per cent in tax on their ‘gain’, based on the highest tax rate.

However, if the investment is classified as a loan no tax would be payable.

Former employees of Bayrock have alleged in a case against the company that the deal was intended to fraudulently evade some $20 million in tax through a disguised sale of partnership interests.

In a press release issued at the time of the initial deal, the FL Group described it this way:

FL Group announces that it has invested $50m in four active US-based real estate development projects alongside Bayrock Group, a US-based international real estate investment and development firm.

These projects are:

• Trump Soho – The development of a 5 star hotel condominium in Soho, Manhattan, in partnership with Donald Trump and the Sapir organization.

• Trump Lauderdale – The development of a 5 star hotel condominium in partnership with Donald Trump situated on Fort Lauderdale beach.

• Whitestone New York – The development of 13 acres of land located along the east river in Whitestone, Queens. Bayrock Group plans to build a number of luxury homes and town homes on this land.

• Camelback – The development of a 5 star hotel and residential condominium in Phoenix.…

Commenting on the new venture, Hannes Smárason, CEO of FL Group said: “This is a very exciting venture, which highlights FL Group’s continued desire to take advantage of new and unique opportunities. The real estate market is an exciting, strong and competitive sector with great growth potential. We look forward to exploring this area with such a distinguished partner as Bayrock Group both in the US and internationally when the possibilities arise. ”

Tevfik Arif Chairman of Bayrock Group commented:

“We are delighted to develop a partnership with FL Group and secure the support of a financial partner with such excellent expertise. We look forward to working with the first-rate team.”

And this is where it gets even more interesting: who is Tevfik Arif, this man with whom Hannes Smárason is issuing press releases? We turn to recent reporting (and thanks are due yet again to Mike the Mad Biologist for his link to the story) by James Henry in The American Interest:

Exhibit A in the panoply of former Trump business partners is Bayrock’s former Chairman, Tevfik Arif (aka Arifov), an émigré from Kazakhstan who reportedly took up residence in Brooklyn in the 1990s. Trump also had extensive contacts with another key Bayrock Russian-American from Brooklyn, Felix Sater (aka Satter), discussed below.8 Trump has lately had some difficulty recalling very much about either Arif or Sater. But this is hardly surprising, given what we now know about them. Trump described his introduction to Bayrock in a 2013 deposition for a lawsuit that was brought by investors in the Fort Lauderdale project, one of Trump’s first with Bayrock: “Well, we had a tenant in … Trump Tower called Bayrock, and Bayrock was interested in getting us into deals.”

According to several reports, Tevfik Arif was originally from Kazakhstan, a Soviet republic until 1992. Born in 1950, Arif worked for 17 years in the Soviet Ministry of Commerce and Trade, serving as Deputy Director of Hotel Management by the time of the Soviet Union’s collapse.10 In the early 1990s he relocated to Turkey, where he reportedly helped to develop properties for the Rixos Hotel chain. Not long thereafter he relocated to Brooklyn, founded Bayrock, opened an office in the Trump Tower, and started to pursue projects with Trump and other investors.

Tevfik Arif was not Bayrock’s only connection to Kazakhstan. A 2007 Bayrock investor presentation refers to Alexander Mashevich’s “Eurasia Group” as a strategic partner for Bayrock’s equity finance. Together with two other prominent Kazakh billionaires, Patokh Chodiev (aka “Shodiyev”) and Alijan Ibragimov, Mashkevich reportedly ran the “Eurasian Natural Resources Cooperation.” In Kazakhstan these three are sometimes referred to as “the Trio.”

The Trio has apparently worked together ever since Gorbachev’s late 1980s perestroika in metals and other natural resources. It was during this period that they first acquired a significant degree of control over Kazakhstan’s vast mineral and gas reserves. Naturally they found it useful to become friends with Nursultan Nazarbayev, Kazakhstan’s long-time ruler. Indeed, State Department cables leaked by Wikileaks in November 2010 describe a close relationship between “the Trio” and the seemingly-perpetual Nazarbayev kleptocracy.

You should read Henry’s entire article for more detail on these complex linkages — between Smárason and Bayrock, between FL Group and these (and other) Russian characters, and of course between the Russians and Trump. Here’s a few more teasers to entice you:

There is much more for us to know about Iceland’s “special” relationship with Russian finance. In this regard, there are several puzzles to be resolved.

First, it turns out that FL Group, Iceland’s largest private investment fund until it crashed in 2008, had several owners/investors with deep Russian business connections, including several key investors in all three top Iceland banks.

Second, it turns out that FL Group had constructed an incredible maze of cross-shareholding, lending, and cross-derivatives relationships with all these major banks…This thicket of cross-dealing made it almost impossible to regulate “control fraud,” where insiders at leading financial institutions went on a self-serving binge, borrowing and lending to finance risky investments of all kinds. It became difficult to determine which institutions were net borrowers or investors, as the concentration of ownership and self-dealing in the financial system just soared.

Third, FL Group make a variety of peculiar loans to Russian-connected oligarchs as well as to Bayrock. For example, as discussed below, Alex Shnaider, the Russian-Canadian billionaire who later became Donald Trump’s Toronto business partner, secured a €45.8 million loan to buy a yacht from Kaupthing Bank during the same period…

Fourth, Iceland’s largest banks also made a series of extraordinary loans to Russian interests during the run-up to the 2008 crisis….

Fifth, there are unconfirmed accounts of a secret U.S. Federal Reserve report that unnamed Iceland banks were being used for Russian money laundering.…

Sixth, there is the peculiar fact that, when Iceland’s banks went belly-up in October 2008, their private banking subsidiaries in Luxembourg, which were managing at least €8 billion of private assets, were suddenly seized by Luxembourg banking authorities and transferred to a new bank, Banque Havilland. This happened so fast that Iceland’s Central Bank was prevented from learning anything about the identities or portfolio sizes of the Iceland banks’ private offshore clients. But again, there were rumors of some important Russian names.

Finally, there is the rather odd phone call that Russia’s Ambassador to Iceland made to Iceland’s Prime Minister at 6:45 a.m. on October 7, 2008, the day after the financial crisis hit Iceland…

You really should read the whole thing. But just to finish out the FL Group/Bayrock story, it ends like so many Smárason stories seem to end, in utter emptiness and ruin:

Completed in 2010, the SoHo soon became the subject of prolonged civil litigation by disgruntled condo buyers. The building was foreclosed by creditors and resold in 2014 after more than $3 million of customer down payments had to be refunded. Similarly, Bayrock’s Trump International Hotel & Tower in Fort Lauderdale was foreclosed and resold in 2012, while at least three other Trump-branded properties in the United States, plus many other “project concepts” that Bayrock had contemplated, from Istanbul and Kiev to Moscow and Warsaw, also never happened.

But maybe he’ll do a better job with those Chinese genomes. Like Trump, Smárason and his company are enjoying some pretty good press at the moment.