Installment 1 in this series is here.

To better understand how zombie corporate viking Hannes Smárason shambled out of the destruction of, first, deCODE Genetics and later the entire Icelandic economy, and then re-emerged into the CEOship of WuXiNextCODE in 2015, let’s begin by reviewing the financial history of deCODE. This is partial account of how deCODE raised its operating capital in different ways, from different sources, from its initial incorporation in 1996, to the “grey market” in Iceland a few years later, through its flourishing at the height of the NASDAQ speculative bubble at the turn of the millennium, and then to its bankruptcy in 2009. (The next installment continues the story of post-bankruptcy deCODE.) This is a story of big structures — capital, corporations, markets, legal and economic regulations — but also of how those structures are built and driven in part by individuals and their relationships.

Let’s take a look at the first deCODE Board of Directors, posed stiffly in 1998 against a lava backdrop:

That’s Kári Stefánsson in the middle, of course; I and others have said enough about him elsewhere that I’ll leave him aside for now,, but never forget that he is always in the middle of the picture. (I have to leave out most of the deCODE story in this more circumscribed financial accounting, but you can always buy the book!. And for a more detailed account of some parts of the story, especially regarding the Health Sector Database, see Skúli Sigurdsson’s 2002 article written as these events were still unfolding, “Bioethics Lite™: Two Aspects of the Health Sector Database deCODE Controversy.”) On the far left is Vigdis Finnbogadóttir, a former President of Iceland, who resigned abruptly and somewhat mysteriously from the Board in December 1998, on the eve of the passage of the contentious and eventually unconstitutional Health Sector Database Act. She provided symbolic capital, joining with Kári Stefansson to provide an Icelandic veneer to the story that deCODE was an “Icelandic company.” The rest of the figures here are the first sign of how that’s largely a symbolic phrase: none of the other Directors were Icelandic, but for now I draw your attention only to the man on the far right: Terry McGuire of Polaris Ventures, a Boston area venture capital firm. Polaris and Arch were the U.S. venture capital firms that ponied up the initial $14 million in start-up funds. Mr. McGuire will return at the end of this installment, taking the different legal and symbolic form of a “stalking horse.”

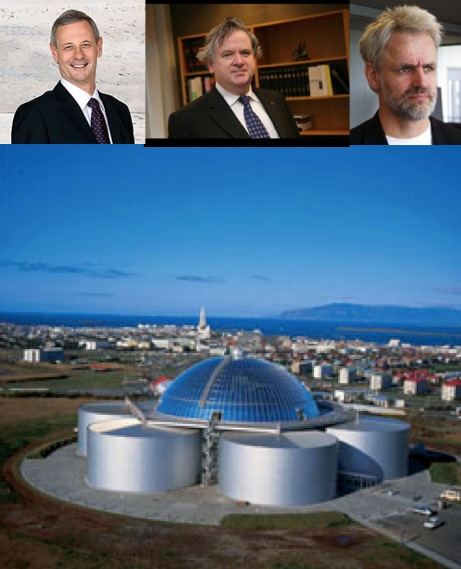

The next big event in the  financial history of deCODE, and the first really public one, was the 1998 swearing of a promise of $200 million to deCODE from the Swiss multinational Hoffmann LaRoche. That’s how it was headlined in the popular and scientific press, anyway; technically the arrangement stipulated that it would be “up to $200 million,” contingent on deCODE reaching a series of research and business milestones, and as we’ll see, the actual amount never got quite up there (in reality it was more like $76 million). But as with so much of the science of genomics, the details and complications get pushed to the background, and the attention-grabbing simplifications — “no one has ever promised $200 million to a startup genomics company before in the entire history of the world!!!” — get pushed to the front. Like many such oaths, this one called for ritualization, with Icelandic Prime Minister Davíd Oddsson, who led the political coalition that would later pass the controversial Health Sector Database legislation, passing the pen between Roche’s Jonathan Knowles and deCODE’s Kári Stefansson as they inked their million-dollar vows in the restaurant in the Perlan dome atop Reykjavik’s geothermal hotwater tanks.

financial history of deCODE, and the first really public one, was the 1998 swearing of a promise of $200 million to deCODE from the Swiss multinational Hoffmann LaRoche. That’s how it was headlined in the popular and scientific press, anyway; technically the arrangement stipulated that it would be “up to $200 million,” contingent on deCODE reaching a series of research and business milestones, and as we’ll see, the actual amount never got quite up there (in reality it was more like $76 million). But as with so much of the science of genomics, the details and complications get pushed to the background, and the attention-grabbing simplifications — “no one has ever promised $200 million to a startup genomics company before in the entire history of the world!!!” — get pushed to the front. Like many such oaths, this one called for ritualization, with Icelandic Prime Minister Davíd Oddsson, who led the political coalition that would later pass the controversial Health Sector Database legislation, passing the pen between Roche’s Jonathan Knowles and deCODE’s Kári Stefansson as they inked their million-dollar vows in the restaurant in the Perlan dome atop Reykjavik’s geothermal hotwater tanks.

Not even the wildest speculators among us then would have imagined that Oddsson would go on to become a central figure in an even larger financial disaster, doing his part as chief governor of the Icelandic Central Bank to bankrupt the entire nation. But that is getting ahead of the story.

So by the late 1990s, with some venture capital and some milestone payments from Roche, deCODE continued to leverage mostly mythical images of Iceland and the Icelandic population into corporate value. With no scientific publications (those would only come much later), and no other Big Pharma partner aside from Roche, in 1999 deCODE took advantage of a loophole in Icelandic securities laws – a loophole that would later be closed by Icelandic financial authorities in large part because of deCODE’s actions in this period – to secure its next capital boost. This gets complicated, and I am simplifying here, so you should consult Promising Genomics for a fuller, better documented version.

In June 1999, a full year before its stock would be offered to the public on the NASDAQ exchange, deCODE sold 5 million shares of its Series B stock at $7.50 per share to a Luxembourg holding company named Biotek Invest S.A., apparently set up for this and only this function. At the same time, an “oral agreement” was made – and while deCODE, like any other U.S. corporation, was legally a person, one may wonder what mouth it employed to make these kinds of spoken promises — an oral agreement was made that deCODE would be paid twice that amount if two conditions were met: the Luxembourg company had to sell at least half of the shares at $15, and the price in “the Icelandic market” didn’t go below $15 for the 6 months remaining in 1999.

Those two conditions were not only met, they were exceeded: 6,000 transactions were made in deCODE stock at prices between $30 and $65 per share on what was called “the gray market.” (For comparison, later at deCODE’s IPO on the NASDAQ in July 2000, the share price opened at $18, and bubbled briefly to $27; it never approached anything near those earlier prices again.) So in this “grey market” environment, deCODE took in $69 million from the bank accounts of probably hundreds of Icelanders eager to participate in a story of national genomic heroism purveyed by Icelandic TV and newspapers, stories tacitly if not explicitly encouraged by the Icelandic banks, which were buying deCODE stock from the Luxemburg holding company and then selling them to Icelanders.

Some of those Icelandars had gotten relatively rich from the recent licensing of the once-national (and hence “public”) fishing stocks, and were looking for places to invest. Others were your average Icelandic Jóns. James Meek of The Guardian collected some of these grey market stories. “I’d never bought stocks before,” Henrik Jónsson told Meek. Jónsson had bought 5 million króna, or $65,000 worth of deCODE stock at $56 per share in the spring of 2000. “I watched the TV news carefully and saw the stock prices rising consistently. You had stories in the media telling people how high Decode stocks were rising. My heart is crying.”

Even worse was the case of the anonymous E., who had also bought in at the height of the exuberance in the spring of 2000, plunking down 30 million króna – about $400,000 – over three separate occasions. Some of the money he borrowed from the state-owned National Bank, from which he also bought the shares; in that case, E. mortgaged his house. He agreed to buy more from the Agricultural Bank, and arranged another loan with the Bank of Iceland. A day later, the Bank of Iceland cancelled all its loans to buy shares, but the Agricultural Bank would not let E. off the hook. He spent the next month trying to arrange other financing, during which time the share price fell from $64 to $50, but the bank insisted he still pay $64. Meanwhile, the National Bank moved to foreclose on its loan. “I asked them if I could wait at least until the shares rose to $15. The lawyer from the bank said, ‘You must know these shares won’t go up.’ I said, ‘You sold me these shares, telling me they would go up to $100.’ He said, ‘If you’re going to blame us you’d better pay up.’”

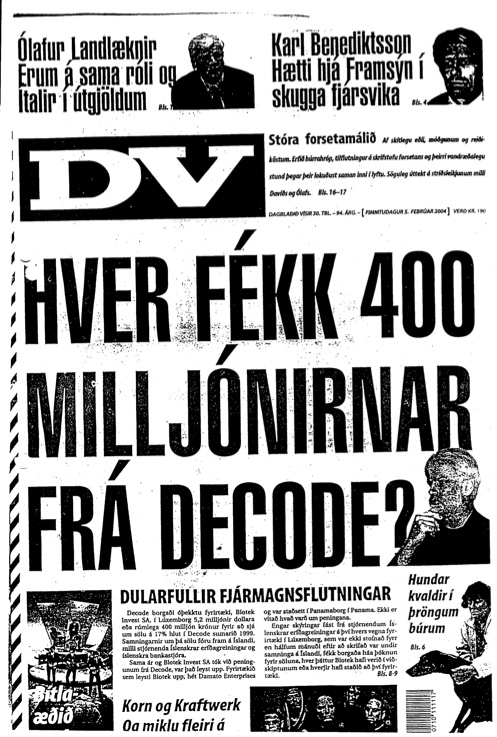

And Biotek Invest S.A.? It was liquidated in December 2000, having existed for barely a year and a half; assets of $5.25 million were transferred to some equally anonymous company called Damato Enterpises Inc. in Panama City, Panama. [In 2016, of course, Panama would be headline material for precisely these kinds of arrangements, and again connected to Iceland.] After the Luxembourg legal notices documenting this baroque story of globalization began coming to light in 2003, the Icleandic newspaper DV ran a cover story on 5 February 2004 that looked like something from the New York Post: “HVER FÉKK 400 MILLJÓNIRNAR FRÁ DECODE?” ran the headline in huge, solid caps – Where did the 400 million kronur from deCODE go? A small picture of Kári Stefansson, rubbing his chin thoughtfully, was inserted next to the question mark. He never responded publicly.

And Biotek Invest S.A.? It was liquidated in December 2000, having existed for barely a year and a half; assets of $5.25 million were transferred to some equally anonymous company called Damato Enterpises Inc. in Panama City, Panama. [In 2016, of course, Panama would be headline material for precisely these kinds of arrangements, and again connected to Iceland.] After the Luxembourg legal notices documenting this baroque story of globalization began coming to light in 2003, the Icleandic newspaper DV ran a cover story on 5 February 2004 that looked like something from the New York Post: “HVER FÉKK 400 MILLJÓNIRNAR FRÁ DECODE?” ran the headline in huge, solid caps – Where did the 400 million kronur from deCODE go? A small picture of Kári Stefansson, rubbing his chin thoughtfully, was inserted next to the question mark. He never responded publicly.

[Here are the documents related to Biotek Invest SA: [biotek invest sa bilan 22.12.2000 biotek invest sa nomination d un liquedateur 21.12.2000 biotek invest status 4.8.1999 biotek invest status coordennes – modifications de statuts 6.8.1999 ]

Now we go from the period of the “grey market” (because of the deCODE events, the regulations governing such sales of securities in Iceland were changed) to the supposedly “white” or colorless market that exists in economic theory. At deCODEs IPO on July 17, 2000, some 11 million shares were sold, grossing $198,720,000. Morgan Stanley, the underwriters, took about $17 million of this as commission and expenses. That’s the colorless story.

Now for a bit of color: what does an underwriter do to earn its commission? In the case of Morgan Stanley in this period, they provided some services to their clients like deCODE which the US Securities and Exchange Commission thought were probably illegal and certainly ethically dubious. The SEC brought action against Morgan Stanley, which decided it would rather settle with the SEC for $40 million rather than try their luck in court. Documents from that settlement between the SEC and Morgan Stanley detail how Morgan Stanley “allocated” future IPO stock offerings only to those investors who had promised to buy stock in other corporations underwritten by Morgan Stanley — companies like deCODE. An email exchange quote in the settlement with the SEC gives a glimpse of how this worked:

“Just for the record . . . despite a less than stellar allocation [a customer] was in buying decode in the aftermarket yesterday. As they said they would. Almost 200m at $28.”

— Morgan Stanley sales representative email to syndicate manager, c. 2000

“I am very aware of their aftermarket. Kudos to them and it will be remembered.”

— Morgan Stanley syndicate manager email to sales representative, c. 2000

(SEC vs. Morgan Stanley, No. 1: 05 CV 00166, United States District Court, District of Columbia, January 25, 2005)

So a sales rep informs his manager that a customer, despite a “less than stellar” allocation, had fulfilled their oral agreement to buy shares of deCODE, “as they said they would.” One almost admires the informal moral economy of promising at work here, as the manager expresses his familiarity with this gentleman’s arrangement to buy some crap or at least “less than stellar” securities, grants his “kudos,” and hints at the promise to come, as they always do in these kinds of gift exchanges: “it will be remembered.” We don;t know how many large investors bought deCODE stock like this, simply because they promised to in order to be invited to future sales served up by Morgan Stanley; we know only that deCODE tucked away about $180 million from their IPO.

In retrospect, we are able to see that deCODE’s timing was perfect, menaing incredibly lucky, since it probably could not have raises so much public biocapital at any other time in recent history before or since. The spring and summer of 2000 saw the briefest, largest, and most intense wave of speculation in the biotech market, with almost twice as many IPOs closed as at any other time in the ten years before or since, generating almost twice the size of step-up in a company’s valuation than any other time before or since:

Source: “Beyond the biotech IPO: a brave new world,” Bruce L Booth, Nature Biotechnology August 2009; doi:10.1038/nbt0809-705.

But here’s what the next 8 eight years looked like for deCODE’s market valuation:

After the cresting of the NASDAQ biotech wave in 2000, deCODE brokered a few more deals with Big Pharma – with Roche of course, in some new agreements that brought in an actual, not merely promised, $50 million spread over five years, and an arrangement with Merck, putting about $9 million per year for three years on the table. Later a contract with the NIH added another dollop of $5 million per year for five years. But those were quite modest revenues for a corporation burning through millions of dollars per month, although together with the biocapital amassed from the grey market and the slightly-less-grey-but-far-from-white IPO, it helped keep deCODE going.

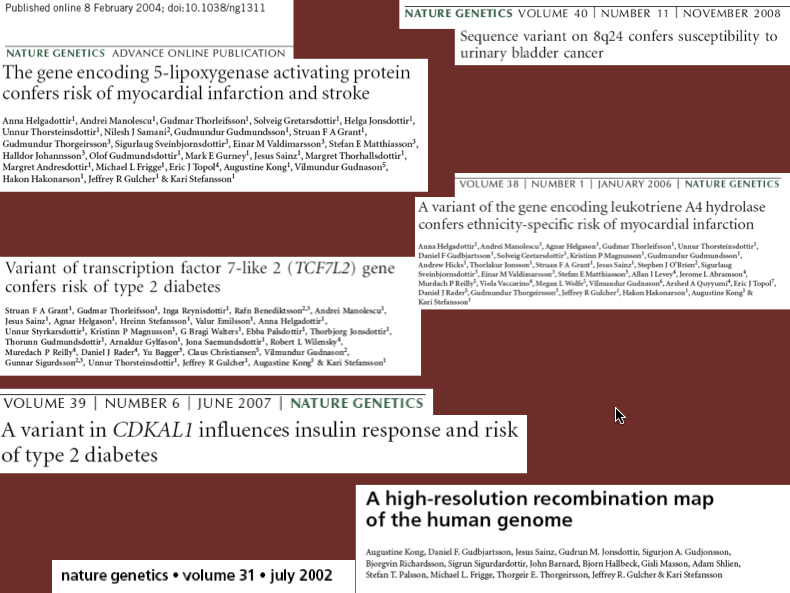

And these arrangements functioned as cultural biocapital as well, and helped produce other forms of cultural biocapital as well, namely scientific publications.  For the first time in its financially lucrative history, deCODE actually began converting dollars consumed into scientific text communicated, securing a number of well-respected publications in noteworthy journals on multiple complex conditions from diabetes to myocardial infarction to prostate cancer. It was finally delivering on some of its promises.

For the first time in its financially lucrative history, deCODE actually began converting dollars consumed into scientific text communicated, securing a number of well-respected publications in noteworthy journals on multiple complex conditions from diabetes to myocardial infarction to prostate cancer. It was finally delivering on some of its promises.

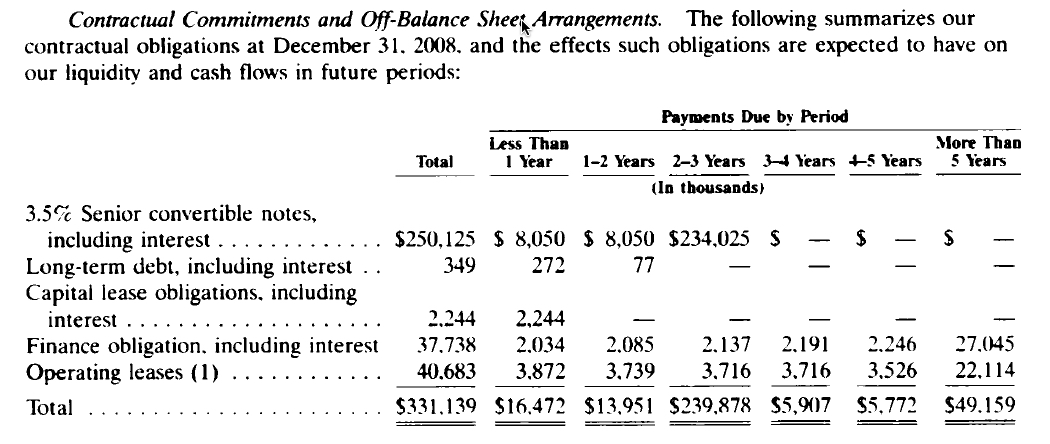

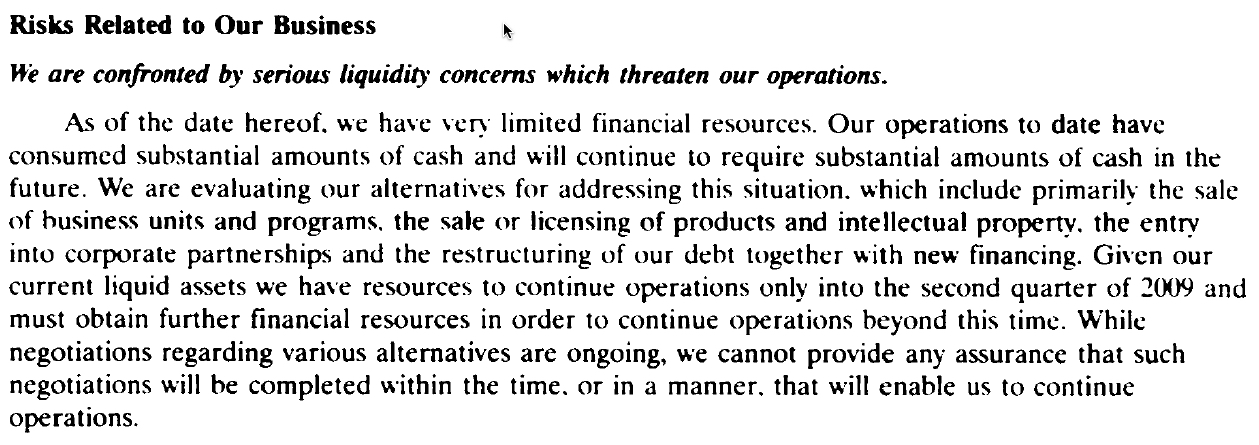

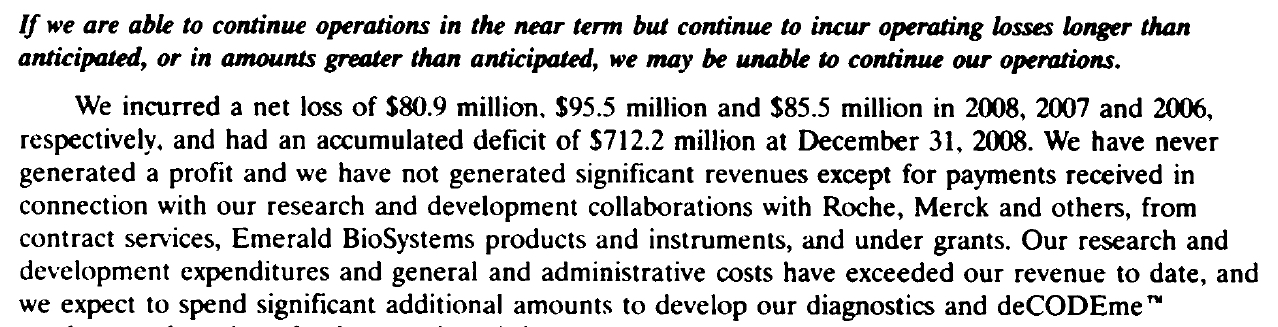

At the same time, however, the bank account was being depleted, and deCODE was again banking on promises, this time in the form of debt. The risk disclosure section of its SEC filings was becoming longer and grimmer, and their 10-K annual report filed with the U.S. Securities and Exchange Commission was downright dismal. The agreements with Roche, Merck, and the NIH provided only a small and shrinking percentage of revenues. DeCODE issued $150 million in debt against its stock value in 2004, and borrowed another $80 million in 2006. So it was paying about $8 million in interest per year, with a final payment in full of $234 million coming inescapably due in 2011.

All told, by the end of 2008 deCODE had eaten nearly three-quarters of a billion dollars in debt, including a $33 million dollar “auction rate security” investment with by then defunct Lehman Brothers, which had already lost $20 million of its value and has got to be pretty near worthless now. Even its remaining relative bright spot, the consumer ancestry and disease-risk testing service deCODEme, had to have its risks and uncertainties narrated to the SEC. And while deCODEme was indeed bringing in increasing revenue, those increases were offset by the increasing “costs of revenue” in the form of chemical sand reagents, advertsing and marketing, and also offset by decreasing “employee compensation” due to “decreased headcount.”

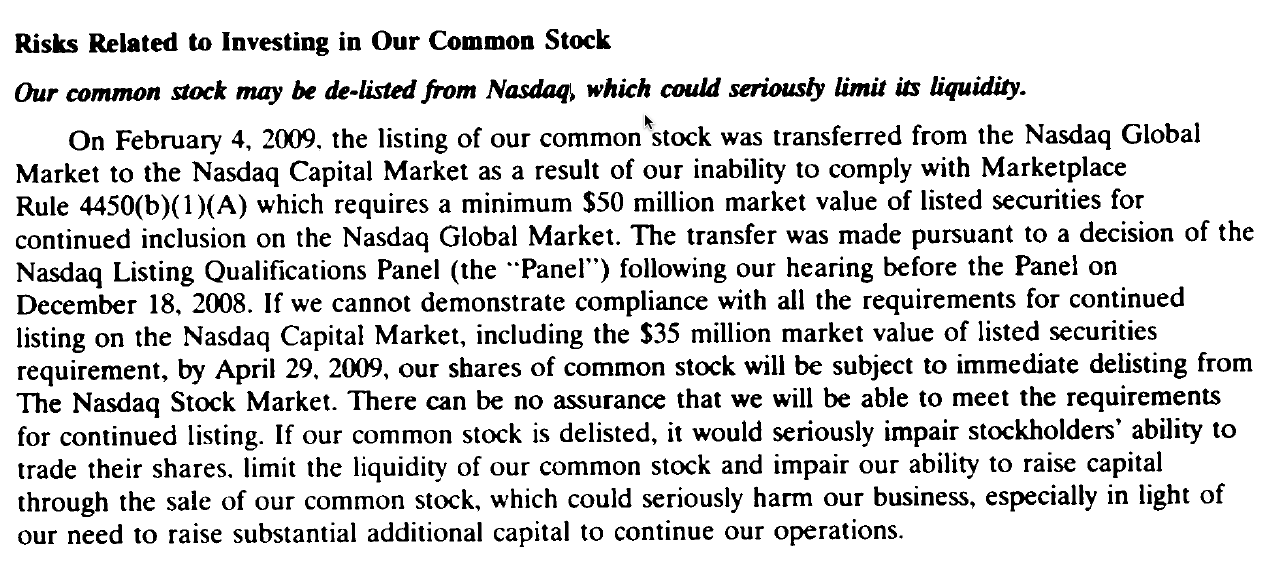

Things went from bad to worse. DeCODE stock, plummeting faster than both the NASDAQ general index and its biotech index, was now trading under a dollar per share and was delisted from the NASDAQ global market.

Things went from bad to worse. DeCODE stock, plummeting faster than both the NASDAQ general index and its biotech index, was now trading under a dollar per share and was delisted from the NASDAQ global market.

By the winter of 2008-2009, not only was the entire Icelandic economy in the toilet, as the metaphor aptly goes, but men could literally piss on the icons of the once highest flying Icelandic financial speculators in the urinals of Reykjavik.

By the winter of 2008-2009, not only was the entire Icelandic economy in the toilet, as the metaphor aptly goes, but men could literally piss on the icons of the once highest flying Icelandic financial speculators in the urinals of Reykjavik.

That’s former deCODE Chief Financial Officer Hannes Smárason in the second urinal from the right, although he mostly ended up there due not to his deCODE position but to his later involvement in the scandalous investment company FL Group. [See installment 4 of this series.] Hannes Smárason also got iconized as that dressed-up waste receptacle that we saw back in installment 1.

In January 2009, street protestors endured the only police tear gassing to occur in Reykjavik since the 1949 anti-NATO riots, and eventually brought down the government.

Davíd Oddsson, who as Prime Minister ten years earlier had handed deCODE so much more than the pen used to ink the $200 million dollar promise with Roche, had gone on to help unleash speculative forces throughout the entire Icelandic economy as one of three governors of its Central Bank. Despite the line-up like quality of Time’s photograph,Davíd Oddsson was never arrested.

Davíd Oddsson, who as Prime Minister ten years earlier had handed deCODE so much more than the pen used to ink the $200 million dollar promise with Roche, had gone on to help unleash speculative forces throughout the entire Icelandic economy as one of three governors of its Central Bank. Despite the line-up like quality of Time’s photograph,Davíd Oddsson was never arrested.

He did, however, hunker down at the Central Bank, refusing to resign or show any sign of repentance or regret, and forcing the Icelandic Parliament to re-legislate the entire Central Bank structure without him in it.

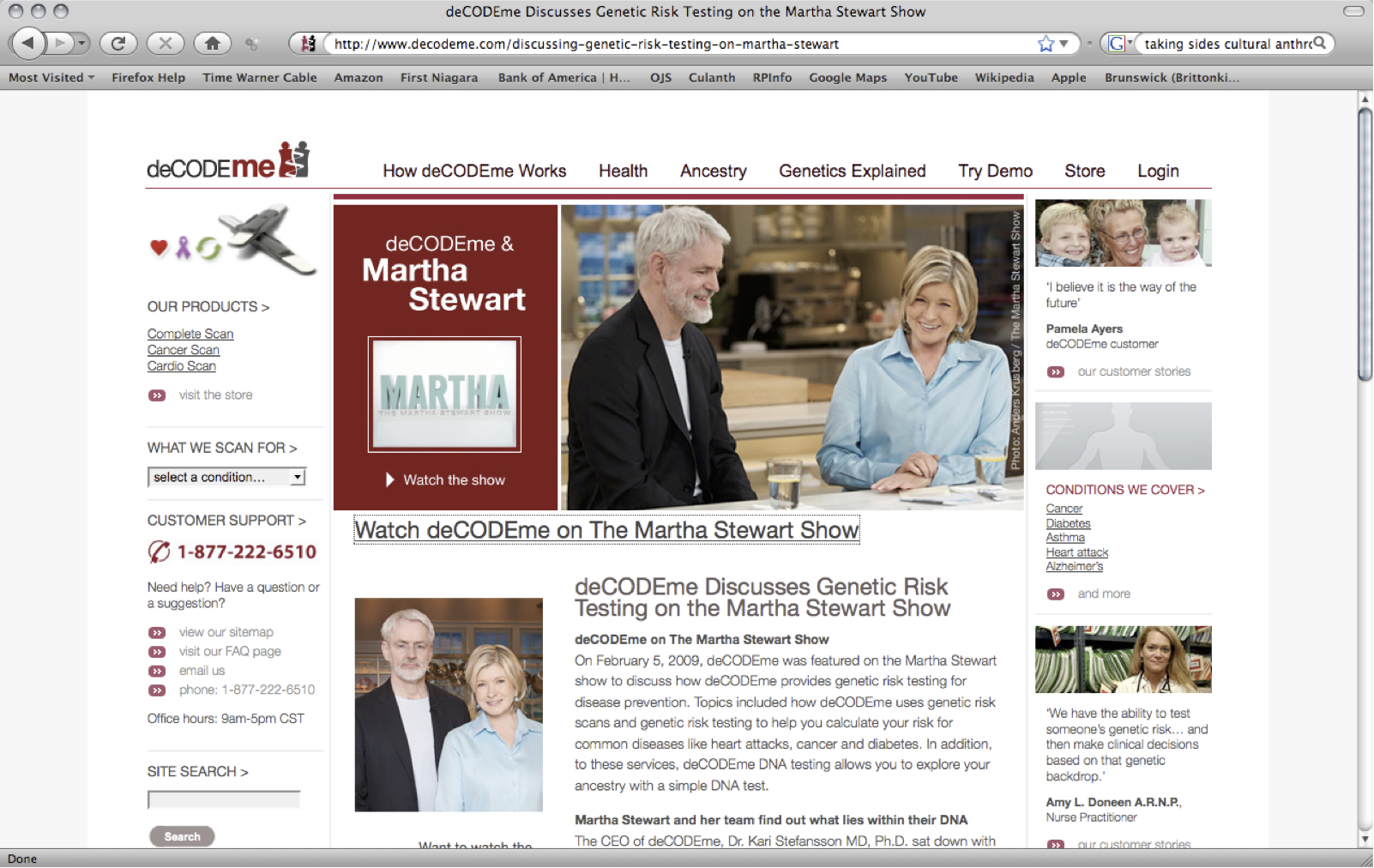

At more or less precisely the same time that Oddsson was holed up at the Central Bank, in one of those fortuitous gifts of history to the ethnographer. Kári Stefansson was again performing his biocelebrity status, promoting the deCODEme services on the TV show of not only the convinced, but convicted, biotech inside trader, Martha Stewart.

So as an avid ethnographic reader of the genomic economy and SEC filings, I was hardly surprised when deCODE filed for bankruptcy in November 2009. And here is where Terry McGuire, the venture capitalist who started this circulatory game of consumption back in 1996. and Polaris Ventures come back into the story again, this time as a “stalking horse,” a term in bankruptcy proceedings drawn from a Native American practice of standing behind a horse, out of the sight of the animal you are hunting. McGuire and Polaris had set up a new holding company, called Saga Investments (they never miss an Icelandic trick), which they then hid behind, in plain sight, ready to pick off whatever deCODE assets remained from the bankruptcy proceedings before anyone else had a shot at them. And that takes us to the next installment.